%201.png)

Why We Passed on a $6.75M Small Bay Industrial Deal in Denver

The property checked nearly every box. The seller's pro forma didn't survive our underwriting.

A shallow bay industrial complex near the I-76/I-270 interchange in Denver's Commerce City submarket came across our desk recently. Five buildings, 45,640 square feet, 52 individually metered suites, 94% occupancy per the broker's marketing materials, and direct freeway access. On paper, it reads like what we look for in our small bay industrial acquisitions.

The seller was asking $6.75 million at $147.90 per square foot, projecting a path from a 4.05% entry cap to a 7.68% pro forma stabilization.

We walked away. Here is the full underwriting breakdown behind that decision.

What Made This Small Bay Deal Look Attractive

Let's be fair to the deal. The fundamentals of the asset itself are solid.

It sits in an industrial-zoned corridor within Denver's Commerce City submarket, near the I-76 and I-270 interchange. The kind of location where automotive shops, home service contractors, and trade businesses want to be. Small bay space averaging 877 SF per suite with 16-foot clear heights is in strong demand and genuinely undersupplied in most major metros. Among comparable properties under 50,000 SF in Commerce City, vacancy sits at just 4.8% (CoStar).

The 52 units are already individually metered for gas and electric across two phases. That is a significant capital expense already absorbed. Individual metering typically costs $10,000 to $15,000 per unit when done from scratch. On a 52-unit property, that represents $520,000 to $780,000 in infrastructure value already in the ground.

The property sits on 3.16 acres, providing adequate parking for the tenant profile. And there is genuine rent growth potential in the roll. Current rents range from $10.68/SF to $20.45/SF across the 52 units, with a weighted average of $14.31/SF. The broader Commerce City submarket averages approximately $12.25/SF across all industrial product types (CoStar). In Jeremiah's view, true small bay space with individual metering and grade-level doors commands $15 to $16+/SF in this market. There is upside in the roll. The question is how much and at what cost to get there.

The bones are there.

"It looks good on the surface, but ultimately it's a trap. You're buying a job." — Jeremiah Boucher, Founder & CEO

Where the Seller's Pro Forma Falls Apart

The seller's package projects reaching $20.00/SF across all 52 units and recovering substantially more operating expenses from tenants. That is the engine behind the 7.68% pro forma cap rate.

The problem: it is being applied to the wrong tenant base and the wrong lease structure.

The Rent Growth Assumption

These are small, owner-operated businesses on annual modified gross leases. A solo plumber. A two-person auto shop. A landscaping crew operating out of a single bay.

The pro forma requires pushing rents from a weighted average of $14.31/SF to a flat $20.00/SF. That is roughly a 40% increase across the portfolio. Some tenants are already near market and would absorb a modest adjustment. Others, particularly those paying $10 to $13/SF, face increases of 50% or more.

For small, local tenants who chose small bay space because it is affordable, that kind of increase is a turnover trigger, not a value creation plan. You could spend two years chasing a rent number that the tenant base simply will not bear.

The Expense Recovery Conversion

At the same time, the seller's pro forma assumes converting the expense recovery structure from its current modified gross basis to one with meaningful triple-net characteristics. Current utility reimbursements total $1,558 annually across the entire property. The pro forma projects $63,710.

That is a 41x increase in expense pass-throughs, layered on top of the rent increases, requiring a wholesale restructuring of the lease basis across all 52 tenants on annual terms. The offering memorandum treats that conversion as a given. In practice, it is a second execution project running alongside the rent growth plan, each compounding the other's turnover risk.

The Expenses the Pro Forma Left Out

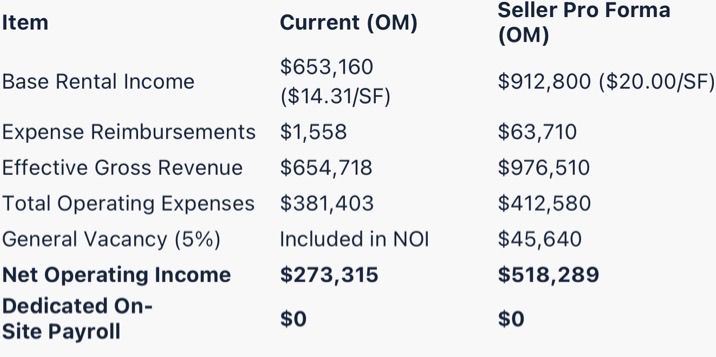

Here is where the analysis gets concrete. The numbers below are taken directly from the broker's offering memorandum.

Operating Statement: Current vs. Seller Pro Forma

Notice the last line: zero dollars allocated to dedicated on-site staffing in either column.

A five-building, 52-unit complex on 3.16 acres of 1985-vintage Class C metal construction does not run itself. You need an on-site presence. Someone to field tenant calls, manage turnover units, handle day-to-day maintenance, and serve as eyes and ears on a 40-year-old industrial park.

The operating statement carries a 5% management fee ($33,683 current) and $35,892 in repairs and maintenance. The management fee covers remote oversight and accounting from a third-party manager. It does not cover the dedicated on-site staff that a property of this scale, age, and tenant count requires. We underwrite that at $40,000 to $50,000 per year at minimum.

How to Read the Cap Rate Math on This Deal

This is the section that determines whether the deal works. Three cap rates, three different stories.

1. The Entry Cap on In-Place Income

The in-place NOI per the offering memorandum is $273,315. On a $6.75 million purchase price, that is a 4.05% cap rate.

That is what you are buying: a 4% yield on today's income before any value-add execution.

2. The Adjusted In-Place Cap (With Real Staffing Costs)

Add $40,000 to $50,000 in realistic on-site payroll and the adjusted in-place NOI drops to roughly $223,000 to $233,000. At $6.75 million, the real in-place yield falls to approximately 3.3% to 3.5%.

You are paying a sub-4 cap for what the property actually produces today with proper staffing.

3. The Realistic Stabilized Cap (Best-Case Execution)

Even if you execute every rent increase the seller projects, absorb the 41x increase in expense recovery, restructure all 52 leases, and staff the property properly, the realistic stabilized NOI lands around $450,000 to $460,000.

On a $6.75 million basis, that is a 6.7% to 6.8% stabilized yield.

The Verdict on the Spread

You are buying at a sub-4 cap on in-place income for the right to execute a business plan that, in the best case, produces a 6.7% to 6.8% stabilized yield. That spread is not wide enough for the execution risk, the capital needs, the lease restructuring complexity, and the turnover probability built into this deal.

What We Would Need to Make This Deal Work

The fundamentals of the asset are real. The location is real. The demand is real. This is not a bad property. It is a mispriced one.

For a deal like this to work, accounting for the execution risk, the capital needs on a 40-year-old metal building, the management intensity of 52 individual tenants, and the realistic rent ceiling for this tenant profile, we would need to acquire it somewhere between $4 million and $5 million.

At that basis:

• The entry cap on adjusted in-place income moves above 5%

• There is enough margin to absorb turnover during the rent growth execution

• You can staff the property properly without compressing the yield

• The stabilized return justifies the illiquidity and the execution complexity

• The exit math works at a realistic disposition cap rate

At $6.75 million, you are paying for the pro forma projection, not the operational reality. That gap is where investors get hurt.

Three Questions Every Small Bay Investor Should Ask

This deal illustrates a broader set of questions that apply to any small bay industrial acquisition. Before running the numbers, ask:

1. Does the pro forma match the tenant? A $20/SF rent target works for a national tenant on a five-year NNN lease. It does not work the same way for a solo contractor on a month-to-month modified gross lease in a Class C park. The rent number has to be achievable for the tenant who will actually sign the lease.

2. Does the expense model include real people? A management fee covers the back office. A 52-unit property across five buildings requires a front-of-house presence. If the operating statement does not include dedicated on-site payroll, add it. Then re-run the cap rate.

3. Is the entry basis priced for execution or for the exit? If the seller's ask price only works under fully realized pro forma assumptions, you have no margin for error. The basis should make sense on current income. The upside is what you earn through execution, not what you pay for at the closing table.

These three filters are part of how we underwrite every deal at Patriot Holdings. They are also why roughly 97% of the deals we review never make it into Fund V.

Our Verdict

Strong asset, wrong price.

The seller's pro forma assumes aggressive rent growth from a $14.31 weighted average to $20.00/SF, a 41x increase in expense recovery requiring wholesale lease restructuring, and zero dedicated on-site payroll for a five-building, 52-unit complex built in 1985. None of those assumptions are realistic for this tenant profile, lease structure, or property scale.

The entry cap on in-place income is 4.05%. Adjusted for real staffing costs, it drops below 3.5%. Even under fully realized pro forma conditions, the stabilized yield is 6.7% to 6.8% on a $6.75 million basis. Not enough margin.

We would be buyers at $4 million to $5 million. At $6.75 million, you are not buying a cash-flowing investment. You are buying a job.

Every deal we evaluate sharpens our underwriting discipline. The ones we pass on are often more instructive than the ones we close. This is part of our ongoing Why We Passed series, where we show our work on the deals that don't make the cut.

Interested in how we think through small bay industrial acquisitions? Have a deal you would like us to evaluate? Contact our team.

Patriot Holdings is a vertically integrated real estate investment and operating company focused on manufactured housing communities, self-storage, and small bay industrial across secondary U.S. markets. Founded by Jeremiah Boucher, the firm has completed $500M+ in transactions across 100+ assets in 35+ states over 17+ years. Fund V is actively deploying capital across all three asset classes and is entering its final allocation window.

This analysis reflects Patriot Holdings' independent underwriting assessment based on information available at the time of review, including the broker's offering memorandum and our own market experience. Our assumptions, projections, and conclusions may differ from those of other qualified operators, investors, or the seller, who may possess material information not available to us. Reasonable professionals can and do reach different conclusions when underwriting the same asset. This content is shared for educational and informational purposes only and does not constitute investment advice or a judgment on the seller, the broker, or any party involved in the transaction.

.jpg)