%201.png)

Cedar Hills Manufactured Home Community: 4.64x Equity. Creative Structuring that Made the Deal.

In December 2017, I acquired a two-community manufactured home portfolio in Harrisonburg, Virginia for $2,400,000. Cedar Hills I at 99 lots. Cedar Hills II at 38 lots. 137 total, all occupied, $280 per month lot rents at acquisition, and a seller I had spent three years earning the trust of before he agreed to terms.

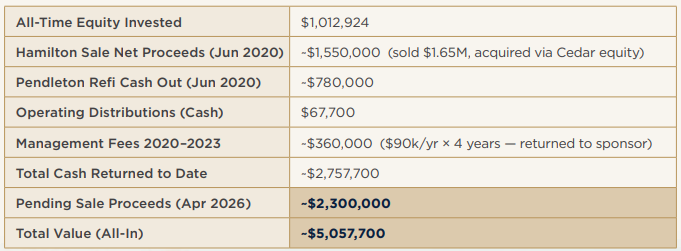

Against $1,012,924 in total equity invested over the life of the deal ($427,498 equity required upon acquisition), Cedar Hills generated approximately $5,057,700 in combined cash returned and exit proceeds. That is a 4.64x equity multiple, 5.0x including management fees and related sponsor distributions. This translated into an estimated IRR of 50% on a conservative floor basis.

The numbers are worth knowing. The structure behind them is what matters.

(Source: Cedar Hills case study, Patriot Holdings, March 2026)

Deal Snapshot

The Acquisition: Three Years Before a Price Was Agreed

I first met the seller, Ron, in August 2016. The parks had been in his family for decades: 137 total occupied lots, $280/month lot rents, no vacancies for 20 years, and a location in Harrisonburg that produced consistent housing demand regardless of economic conditions. Proximity to James Madison University added a durable demand layer that reinforced the thesis.

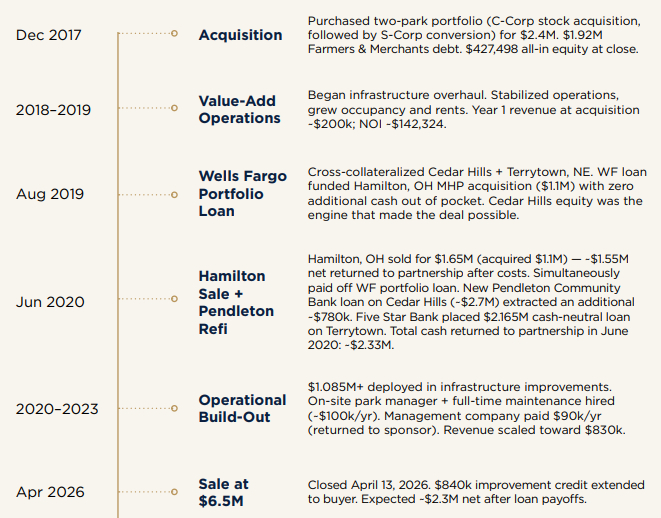

The structure of the deal is what made the transaction possible. The parks were held inside a C-Corp. A standard asset purchase would have triggered depreciation recapture and capital gains at the entity level, creating a double-tax outcome that made the economics unworkable for Ron. The solution was a stock purchase: Patriot acquired the shares of the family corporation, not the underlying real property. Ron solved his tax problem.

Patriot accepted a specific cost in exchange. A stock purchase preserves carryover basis rather than stepped-up basis, meaning no fresh depreciation on the acquired real property. That was the trade we made to close the deal.

Post-closing, we converted the acquired entity from C-Corp to S-Corp. The S-Corp conversion eliminated entity-level tax on operating income going forward, preserved single-level taxation through the hold, and allowed depreciation on the acquired assets and on new capital improvements to pass through to shareholders. The conversion didn't recover fresh depreciation on the purchase price, but it recovered most of the ongoing tax efficiency that would otherwise have been lost inside a C-Corp hold.

Three years of relationship-building produced the creative structure that made the transaction viable for both sides. The agreed purchase price was $2,400,000. Financing of approximately $1,920,000 came from Farmers and Merchants Bank. All-in equity at close was $427,498.

(Source: Cedar Hills case study, Patriot Holdings, March 2026)

"Meeting with the owner Ron over three years is what allowed us to build this relationship, and it was a really good win. The key to the transaction was buying the stock units of the family's corporation." - Jeremiah Boucher, Founder and CEO, Patriot Holdings

The Capital Timeline

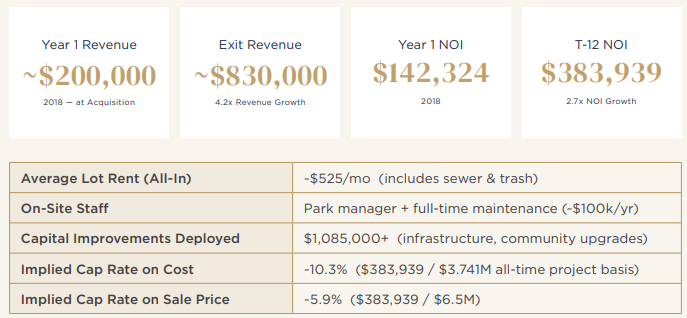

Operating Performance

The Cap Rate Math

Two cap rates matter here. Both are explicit.

Implied Cap Rate on Cost: $383,939 T-12 NOI divided by $3,741,000 all-time project basis equals 10.3%.

Implied Cap Rate on Sale Price: $383,939 T-12 NOI divided by $6,500,000 sale price equals 5.9%.

Source: Cedar Hills case study, Patriot Holdings, March 2026. Derived math calculated from stated figures.

Total Return Summary

Key Takeaways for Investors

1. Equity is a tool, not just a return. The cross-collateral structure converted built-up equity into a zero-cash acquisition engine. The April 13 exit is not the only moment value was created.

2. Understand the seller's problem before negotiating price. The stock purchase was the deal. Without it, there was no transaction. Three years of relationship-building produced the creative structure a first-call negotiation never would have.

3. Operational infrastructure compounds. Revenue grew from $200,000 to $830,000 through full-time on-site staffing, $1,085,000+ in capital improvements, and eight years of consistent management. Not financial engineering. This value creation is the result of execution and creative structuring over the course of the hold.

Three Questions Every MHC Investor Should Ask

1. How does utility infrastructure affect long-term operating cost?

Public utilities transfer maintenance responsibility to the municipality. Private utilities (well water, septic) transfer it to the operator. The difference shows up in your expense line every year and in large capital events when systems age. Underwrite this carefully before close, not after.

2. What structure does the seller actually need, and how does that affect your basis?

Legacy MHC sellers frequently have tax-efficiency requirements that constrain deal structure. A stock purchase, installment sale, 1031/721 exchange accommodation, or post-acquisition S-Corp conversion can be the difference between a deal that closes and one that does not. Understanding what the seller needs before negotiating price often produces better outcomes for both sides. Understanding what structural options you have after closing expands the outcomes further.

3. How does built-up equity create optionality within a portfolio?

In isolation, Cedar Hills was a strong deal. Within a portfolio, it funded a zero-cash acquisition in Ohio, accelerated capital return by years, and ultimately produced a ~5.0x combined equity multiple. The cross-collateral structure was only possible because Cedar Hills had been operated correctly and had built real equity. Equity in one asset is potential capital in another.

Verdict

Why This Matters for Fund V

The Cedar Hills framework is how we approach every manufactured home community in Fund V: relationship-sourced origination, disciplined structure, operational infrastructure built to last, and capital recycling that aims to create returns before the exit ever closes. Fund V has acquired 17 properties as of March 2026, with approximately $53.7M in total cost basis, targeting $75M to $95M at full deployment. The final allocation window closes August 1, 2026.

If you would like to learn more about our manufactured housing investment strategy or discuss current Fund V allocation, we welcome the conversation.

Schedule a call with the Patriot Holdings team

Read The Full Case Study

About Patriot Holdings

Patriot Holdings is a commercial real estate private equity platform with 17+ years of operating history, $500M+ in transaction volume, and 100+ assets acquired across 18+ states. Zero investor principal lost across all funds to date. Current flagship offering: Fund V, a 506(c) private offering focused on self-storage, small-bay industrial, and manufactured housing communities.

.png)